Five of the most important facts everyone gets wrong about Social Security

There’s no denying that Social Security is confusing. But many people — including those close to retirement age — struggle to grasp even the basics.

Only 28 percent of people passed a 10-question true or false quiz on Social Security benefits, according to a study by MassMutual Life Insurance Company. Just one person out of the more than 1,500 who took the test answered all 10 questions correctly. (A passing score was answering eight out of the 10 questions correctly.)

The report shows that people are not only confused about when they should start collecting Social Security to get the most out their benefits, they may not fully understand what they’re entitled to or how other decisions may affect their benefits and taxes. Here are some of the most fundamental things many people got wrong.

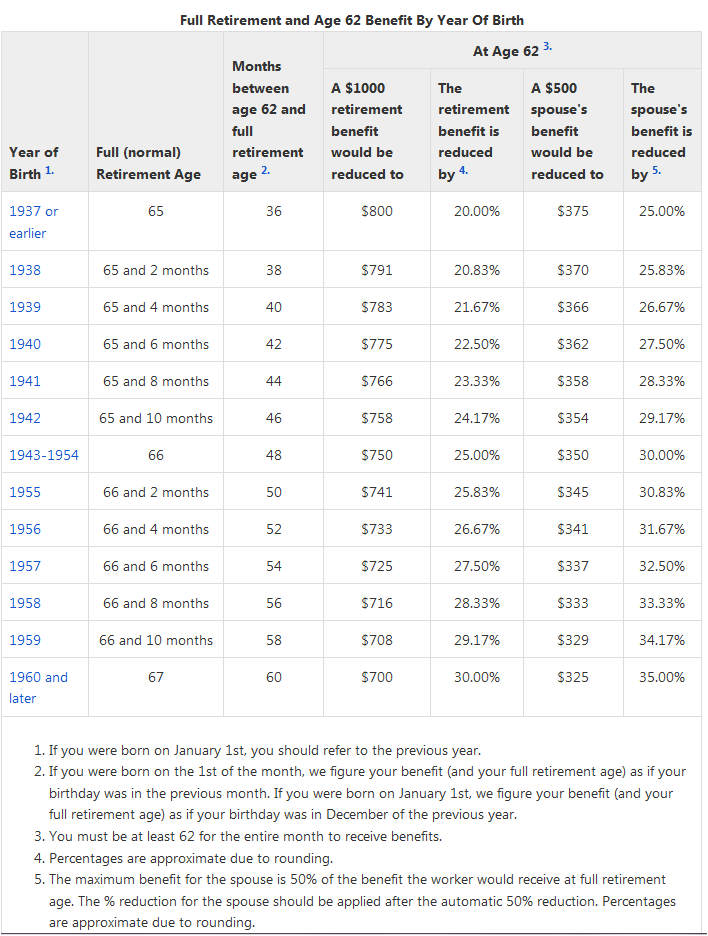

The official retirement age is not 65.

More than 70 percent of people surveyed said they thought the full retirement age was 65. That used to be the case, but now a person’s full retirement age, or the age at which they can start collecting full retirement benefits, varies depending on the year they were born. The full retirement age is 66 for people born between 1943 and 1954 and it gradually increases to 67 for people born in 1960 or later. Getting the official retirement age right is important because people who collect benefits early get reduced monthly checks and those who wait beyond their retirement age to collect can receive 8 percent more for every year that they delay. (Check the table below from the Social Security Administration.)

Working can reduce your benefits.

Most people, about 55 percent, thought it was fine to keep working while receiving retirement benefits, regardless of age. But they overlooked that people who haven’t reached their full retirement age yet could see Social Security benefits reduced if they earn above a certain amount. For instance, people born between 1943 and Jan. 1, 1955 will have $1 deducted from their benefits for every $2 they earn above $15,720 if they’re younger than their full retirement age. The money isn’t lost forever. It gets added on later after they reach their full retirement age. (People who work past their full retirement age can keep all of their benefits, no matter how much they make.)

You can collect retirement benefits from an ex.

Only 45 percent of people knew that they could collect Social Security spousal benefits after getting divorced. This is generally true if the two people were married for at least 10 years and the person looking to collect their former spouse’s benefits has not re-married. That ex could even collect the spousal benefits while they put off their own Social Security to take advantage of delayed retirement credits.

You don’t need to be a citizen to collect.

About 75 percent of the people surveyed wrongly said only citizens can collect Social Security. Workers are generally eligible to receive Social Security benefits after 10 years of working and paying taxes into the system. That’s true regardless of whether or not you’re a citizen. Workers with legal residence status risk leaving money on the table if they overlook this rule and fail to collect benefits they’ve earned.

Social Security will likely be a huge part of your retirement plan.

In addition to the quiz, people were asked about how much they expect to rely on Social Security in retirement. The majority, 63 percent, said they expect Social Security to be around when they retire, but about 44 percent said they expect to rely more on their own savings in retirement.

But 52 percent of married couples and 74 percent of single people receiving retirement benefits get more than half of their income from Social Security.

That means any confusion over how the program works could substantially affect a person’s retirement plan, advisers say. “If they get this Social Security decision wrong, I think all of the other decisions about their other assets will be either be skewed or they won’t fit,” says David Freitag, financial planning consultant MassMutual. “It’s important to know the specifics.”

In 2014, over 59 million Americans will receive almost $863 billion in Social Security benefits.

Social Security is the major source of income for most of the elderly.

- Nine out of ten individuals age 65 and older receive Social Security benefits.

- Social Security benefits represent about 38% of the income of the elderly.

- Among elderly Social Security beneficiaries, 52% of married couples and 74% of unmarried persons receive 50% or more of their income from Social Security.

- Among elderly Social Security beneficiaries, 22% of married couples and about 47% of unmarried persons rely on Social Security for 90% or more of their income.

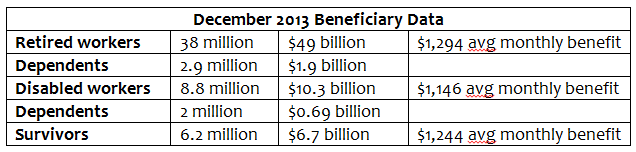

Social Security provides more than just retirement benefits.

- Retired workers and their dependents account for 74% of total benefits paid in December 2013.

- Disabled workers and their dependents account for 16% of total benefits paid in December 2013.

- About 90 percent of workers age 21-64 in covered employment in 2013 and their families have protection in the event of a long-term disability.

- Just over one in four of today’s 20 year-olds will become disabled before reaching age 67.

- 68% of the private sector workforce has no long-term disability insurance.

- Survivors of deceased workers account for 10% of total benefits paid in December 2013.

- About one in eight of today’s 20 year-olds will die before reaching age 67.

- About 96% of persons aged 20-49 who worked in covered employment in 2013 have survivors insurance protection for their young children and the surviving spouse caring for the children.

An estimated 165 million workers are covered under Social Security.

- 51% of the workforce has no private pension coverage.

- 34% of the workforce has no savings set aside specifically for retirement.

-In 1940, the life expectancy of a 65-year-old was almost 14 additional years; today it is about 20.

-By 2033, the number of older Americans will increase from 46.6 million today to over 77 million.

-There are currently 2.8 workers for each Social Security beneficiary. By 2033, there will be 2.1 workers for each beneficiary.

http://www.socialsecurity.gov/

Leave a Reply